Retirement Withdrawal Strategies

There comes a time when investors transition from the accumulation phase of building up assets to drawing from those assets to support living expenses in retirement. In this post, we discuss various withdrawal approaches from retirement and brokerage accounts so you can spend confidently throughout retirement. Before covering a few different retirement withdrawal strategies, let’s review some important guidelines that serve as a framework for these strategies.

Retirement Withdrawal Guidelines

- Minimize Required Minimum Distributions (“RMDs”). Tax-deferred accounts like 401(k)s, 403(b)s, and IRAs are subject to RMDs. The starting age for RMDs has been recently pushed back to 73 or 75 depending on your date of birth. The amount of the RMD is based on your remaining life expectancy, with a higher percentage of the balance required to be withdrawn the older you get. The entire amount withdrawn is taxable at ordinary income tax rates. Ideally, you want to avoid being forced to withdraw an amount above and beyond what you need from those accounts to supplement living expenses and thereby pay unnecessary taxes. An additional side effect of having a large RMD is potentially increasing the Medicare IRMAA (income-related monthly adjustment amount) surcharge on your premiums. Some ways to manage RMDs and their associated taxes at ordinary rates are:

- Qualified Charitable Distributions (“QCDs”). Starting at age 70.5, you can direct a portion or all of your RMD up to $105,000 (index adjusted annually) to charity and have the QCDs be excluded from taxable income.

- Realize the income from tax-deferred accounts while in a low tax bracket. Withdrawals can typically start at age 59.5, before Social Security income hits and RMD age starts. Also consider Roth conversions in low-income years. Conversions can be done at any age and can be an effective strategy for those with large tax-deferred assets and low taxable income.

- Defer Withdrawals from Roth Accounts. Roth assets benefit the most from compounding over long periods of time since they enjoy tax-free growth and tax-free withdrawals. Deferring your Roth withdrawals works well with shrinking future RMDs because money could come from your tax-deferred IRA or 401(k) to fund living expenses before RMD age. If you defer withdrawals from tax-deferred accounts as opposed to deferring withdrawals from your Roth, you might be unnecessarily compounding your future tax liability.

We don’t know where tax rates will be in the future, but we are currently in a relatively low federal individual income tax rate environment. If tax rates increase in the future, Roth assets will be comparably even more valuable. - Build Tax Flexibility. Diversify your taxes through building up different investment account types (tax-deferred, tax-free, and taxable). Refer to our tax-efficient investing post, which includes the characteristics of these three account types.

The main benefit from having three different account types to choose from is the ability to manage your taxable income each year. Maybe you take some time off work and consequently have a lower income than normal. Maybe you unexpectedly receive an inherited IRA or earn more than expected from a side venture, increasing your taxable income. Maybe new tax legislation is passed. Whatever the case, the presence of different account types can help you manage your tax liability each year.

With these guidelines in mind, there are a few different retirement withdrawal strategies depending on your unique situation.

Withdraw From One Account Type at a Time

In perhaps the most traditional retirement withdrawal strategy, retirees withdraw from one account type at a time until each is fully depleted. It starts with taxable accounts, then moves to tax-deferred, then tax-free accounts last.

This strategy is based on the fact that taxable accounts have a “tax drag” year after year from interest, dividends, and capital gains. Tax-deferred and tax-free accounts grow more efficiently because they don’t have that tax drag. However, one way to mitigate the drag is to have low turnover, tax-efficient investments inside taxable accounts.

Taxable accounts also benefit from preferential long-term capital gains rates on sales/withdrawals (0% up to $94,050 in taxable income for married filing jointly in 2024). So, it could make sense for those with large unrealized gains to withdraw from these accounts first to take advantage of the 0% tax rate, as opposed to having the long-term capital gains rates pushed higher from income from Social Security and tax-deferred accounts later on.

What often arises with this traditional strategy is a larger future RMD because the tax-deferred IRAs weren’t touched while taxable assets were spent. This approach also doesn’t keep your tax situation flexible since account types are depleted one by one. While minimizing taxes in the early years of retirement, this strategy may lead to large tax bills later on.

Blended Withdrawals

To lower the overall tax burden and extend the life of your assets, in many cases it makes sense to withdraw from both your taxable accounts and tax-deferred accounts first, then tax-free Roth accounts last. This strategy keeps RMDs down in the future, taxes paid more balanced throughout retirement, and potentially less in taxes paid overall.

Be careful, because too much in tax-deferred IRA withdrawals in the early years of retirement can push your current tax brackets up, defeating the purpose of the strategy. The use of withdrawing some from the taxable account can help keep your current tax brackets from getting too high, while still satisfying living expense needs. The right balance between the two is where income and tax planning can provide tremendous value.

This approach can get closer to following the three withdrawal guidelines than the traditional strategy. It still defers Roth accounts, does better at maintaining tax flexibility, and lessens RMDs. Yet, there’s another strategy that is sometimes even more tax-efficient.

Roth Conversions During the “Gap Years”

The term “gap years” refers to the time after retirement when wages fall but before income in the form of Social Security and RMDs starts. There could be 5–15 years when your taxable income is substantially lower than in your working years.

Called a Roth conversion, this strategy converts some tax-deferred assets to tax-free assets while you are in a marginal tax bracket lower than if you withdrew those tax-deferred assets later on in retirement. Make sure not to convert so much that it drives taxable income (ordinary income and capital gains) into higher marginal tax brackets.

In the lower income years, look at how much more room there is to make a conversion up to the top of the next marginal tax bracket. For example, maybe you dropped to the 12% marginal bracket but have plenty of room before entering the 22% marginal bracket. It could make sense to make a conversion to the top of the 12% bracket.

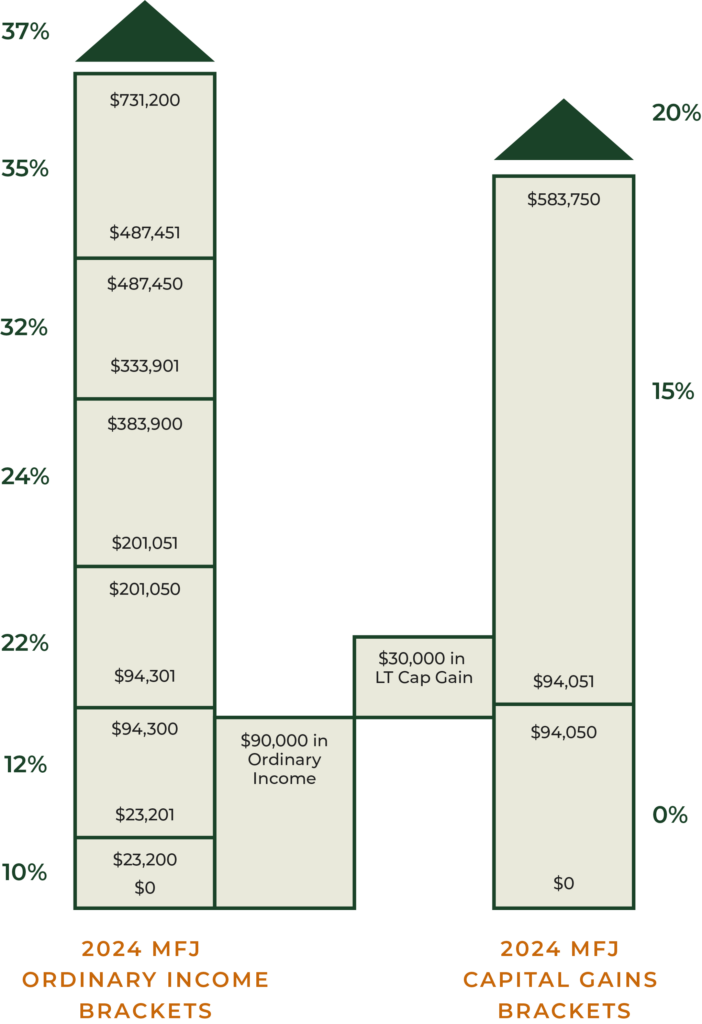

Along with ordinary income brackets, capital gains brackets should be considered. The diagram below shows an important aspect of how these different types of income are taxed. The $90k in ordinary income (this is where Roth conversions would be categorized) is taxed at ordinary rates and is pushing almost all of the $30,000 of long-term capital gains into the 15% bracket.

Source: Verum Partners

Ideally, you want to manage your ordinary income so that more long-term capital gains are taxed in the 0% bracket. So, instead of making a Roth conversion that puts ordinary income at $90,000, maybe you should try to get ordinary income closer to $60,000 to give room for your $30,000 of LTCG to be taxed at 0%. As you can see, it’s not just the standard ordinary income tax brackets that need to be considered when executing this strategy.

After you are done making Roth conversions and living off the taxable brokerage account in the gap years, transition to the traditional or blended withdrawal strategy. The key to this strategy is having a taxable account that can support living expenses in the years the Roth conversions take place.

The overall result is higher taxes in the early years that conversions take place, but lower overall taxes throughout the course of retirement. The Roth account likely becomes the largest of the three account types by the end of retirement thanks to the tax-efficient compounding, the tax-deferred account shrinks early on from the Roth conversions, and there is more after-tax wealth left over. Medicare premiums are likely to be lower over the course of retirement with lower RMDs in the future, but be sure to consider any effects on health care subsidies for those on the Exchange (Health Insurance Marketplace) before Medicare age of 65.

Although this strategy draws on the taxable account quicker, there still remains some tax flexibility going forward, and the Roth conversion was the direct benefit of having tax flexibility in the first place.

Conclusion

Although there are some general guidelines to follow, the withdrawal strategy you choose should be highly personalized based on your financial circumstances. Some considerations include charitable intent, legacy goals, life expectancy, retirement age, size of taxable account, amount of unrealized long-term capital gains, size of tax-deferred accounts, annual living expenses, and other income sources, to name a few.

Maybe you don’t want to leave assets to your children but instead want everything to go to charity—then Roth assets aren’t as attractive to build up and pass on. Maybe you have substantial tax-deferred assets, few Roth assets, live modestly, and plan on retiring early—then Roth conversions might make sense. Maybe you have taxable assets that are highly appreciated and not a lot of tax-deferred assets—then having more of a traditional strategy might be best.

Tax planning is powerful. Work with your financial adviser to help determine the most optimal retirement withdrawal strategy for your nuanced financial situation.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor. The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur. For additional information, please visit: https://verumpartnership.com/disclosures/

Be the First to Know

Sign up for our newsletter to receive a curated round-up of financial news, thoughtful perspectives, and updates.

"*" indicates required fields