Three Phases of the AI Evolution

Artificial Intelligence (AI) is emerging as one of the most transformative technologies in recent history, reshaping financial and labor markets, industries, and the way companies operate. Its impact is already visible in various applications, from automating routine tasks and enhancing customer experiences to driving product innovation and altering capital allocation decisions. As AI continues to evolve, it has the potential to redefine entire business models and give AI-adopting companies a competitive edge. Those who leverage AI are likely to thrive while companies and industries that fail to adapt risk falling behind.

Three Phases of AI

We believe the AI industry will mature in three distinct phases. Each phase of the AI evolution builds on the previous one, creating a cumulative effect that continues to drive change across the global economy. This post explores the three phases in greater detail:

- The Foundation Phase –Establishing the core infrastructure that enables AI to function at scale, including computing power, data centers, and energy infrastructure

- The Platform Phase – The development of platforms and tools that make AI accessible, allowing organizations to integrate AI capabilities into their operations

- The Transformation Phase –Companies and industries apply AI broadly to improve efficiency, enhance products and services, and reshape how businesses operate

The Foundation Phase

The Foundation Phase lays the physical groundwork for the AI transformation and is driven by semiconductor chips, data centers, and energy infrastructure. This is the stage when both the physical and digital groundwork for broad AI integration is established. It enables the training and deployment of advanced AI models that are then used across various industries and applications. As these models grow more capable and complex, they will require more computational power and energy, fueling a global race to build new data centers and upgrade electrical grids to sustain them.

At the core of this phase are semiconductors, particularly graphics processing units (GPUs) and tensor processing units (TPUs). Originally developed for gaming consoles, GPUs are specialized chips designed to perform thousands of simultaneous calculations, making them ideal for training large language models capable of analyzing vast datasets. They now serve as the backbone for AI workloads. TPUs are specialized chips built specifically for common machine learning calculations, especially the repetitive matrix multiplications that power AI models, delivering high speeds and energy efficiency for focused AI workloads, but they are less flexible than GPUs, which can handle a broader mix of tasks.

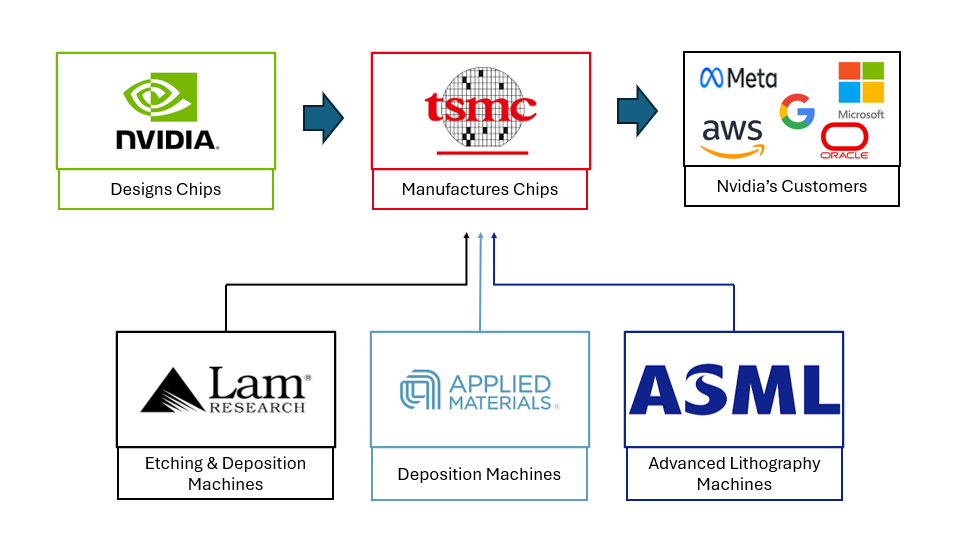

The creation of these chips depends on a global and deeply integrated supply chain. Nvidia Corporation, the leader in AI hardware, designs its chips in the United States but relies on TSMC (Taiwan Semiconductor Manufacturing Company) to manufacture them. TSMC needs highly advanced and precise lithography equipment from ASML, the only company in the world capable of manufacturing extreme ultraviolet machines, which are critical to producing the smallest and most powerful chips. Equipment suppliers such as Lam Research and Applied Materials provide the tools used to etch and clean materials throughout the manufacturing process. This interconnected and fragile supply chain stretches across the globe and is the backbone of the modern AI economy, with each company performing a crucial role in the production of chips.

Semiconductor Supply Chain Flow Chart:

Nvidia’s leadership is built not only on the best-in-class performance of its GPUs but also on its software ecosystem, most notably CUDA. This system allows AI tool developers to optimize their models specifically for their chip’s architecture. AMD (Advanced Micro Devices) remains a primary competitor to Nvidia, producing GPUs that deliver similar performance, and often at lower cost, though its developer ecosystem is less mature. Broadcom also plays an important complementary role by supplying high-speed networking chips that enable fast and reliable data transfer within data centers, as well as their application-specific integrated circuits (ASICs). These highly customized chips are designed for specific advanced inference and other targeted AI workloads, where higher performance and energy efficiency can be achieved at the expense of flexibility compared to general-purpose GPUs.

Once chips are produced, they are deployed in data centers that serve as the engines of artificial intelligence. These facilities house tens of thousands of GPUs and CPUs that train, store, and run the AI models themselves. Cloud providers such as Amazon, Microsoft, and Google continue to invest in building new data centers at a record pace to meet rising demand for computational power.

New generations of AI models have each required more computational power and storage, resulting in larger facilities with greater energy needs. This expansion has made data centers one of the fastest-growing consumers of electricity globally, creating new challenges for utilities and power grids. The surge in energy demand is changing infrastructure investment as AI workloads require significant amounts of electricity to power both computation and cooling systems. To meet growing demand, companies are working with utilities to expand capacity and explore cleaner energy sources, including modular nuclear power, large-scale battery storage, and natural gas turbines.

The combination of AI models, powerful semiconductors, expanding data center capacity, and rising energy production enables the continued evolution of AI. This entire supply chain, from chip design and production to deployment in data centers, ultimately delivers the computational power and storage that platform providers rely on to run AI models and applications at scale. In prior technological revolutions, we have seen a boom-and-bust dynamic in which excitement for investment opportunities within the Foundation phase ultimately led to oversupply or overbuilding of infrastructure. It is too early to know whether the AI boom is at risk for such a scenario, but risks such as changes to future model efficiency could impact the necessity of more infrastructure.

The Platform Phase

The Platform Phase of AI evolution centers on cloud-based platforms and AI tool providers that make it easier for companies to integrate AI into their operations. Major cloud providers like Amazon Web Services, Microsoft Azure, and Google Cloud provide the infrastructure to run AI on a large scale, connecting the chips from Nvidia and AMD with the software and models that businesses rely on. These platforms host AI models capable of understanding natural language, summarizing documents, assisting with decision-making, and research. Various companies such as IBM, Databricks, and cloud providers build tools that help organizations customize and deploy AI solutions, making these capabilities accessible to businesses of all sizes.

Cloud and software providers are making huge investments to meet growing demand and are collectively referred to as hyperscalers. Amazon, Google, and Microsoft are considered the Big Three North American cloud providers and have been allocating tens of billions of dollars to AI-related capital expenditures. These investments support both internal applications, such as automating company workflows, and external products, like Microsoft Copilot, which help clients deploy AI in day-to-day operations. For example, AI-enhanced search engines are now surfacing answers and summaries directly at the top of results pages, giving users faster and more relevant information.

AI agents are beginning to emerge within this phase, representing a new layer of functionality. While standard large language models passively await prompts, AI agents operate actively, planning, reasoning, and executing sequences of tasks with minimal human oversight. They can also be custom-built by the user to handle a specific task based on their needs, allowing businesses to tailor AI to their unique workflows and objectives. For example, AI agents can manage customer service inquiries from start to finish, draft and send routine emails, conduct research across multiple sources, assist with coding projects, or monitor and summarize business data, providing real-time insights. While these agents improve operational efficiency, they also demonstrate how AI’s growing capabilities are shifting from acting as a chatbot to potentially automating roles within the labor force.

By building the infrastructure, software, and tools that make AI practical for businesses, firms in the Platform Phase set the stage for the Transformation Phase. Their work will allow organizations across industries to apply AI strategically to operations, products, and services, accelerating adoption and creating opportunities for greater efficiency and innovation.

The Transformation Phase

The Transformation Phase represents the widespread adoption of AI across the economy, where companies use AI to improve efficiency, products, and services. This phase is still in its infancy, and while its full impact remains uncertain, its influence is already being felt across many sectors ranging from healthcare and finance to consumer services and manufacturing.

In healthcare, AI is changing everything from drug development to patient care. Pharmaceutical companies are using AI to accelerate the drug discovery process by analyzing massive datasets and identifying potential compounds much faster than traditional methods. AI tools can model how drugs will interact with the body before they ever reach human trials, cutting both costs and development time. In patient care, organizations like UnitedHealth Group use predictive analytics to identify at-risk patients and streamline claims processing, while hospitals deploy AI systems for imaging analysis and diagnostics, improving accuracy and reducing wait times. Together, these innovations are helping healthcare organizations deliver better outcomes for patients at lower cost.

In finance, firms are adopting AI to enhance decision-making, manage risk, and improve client service. Banks like JPMorgan Chase use AI to automate contract analysis, detect fraud, and optimize trading strategies, saving thousands of hours of manual work. Asset managers are integrating AI into portfolio management to spot market trends in real time and make more informed investment decisions, while insurers are using machine learning to improve underwriting and claim processing efficiency. These tools not only reduce costs but also give institutions a data-driven edge in decision-making.

In consumer services, companies are using AI to streamline operations and improve customer experience. McDonald’s, for example, has introduced AI-powered voice ordering at drive-throughs, reducing wait times and labor needs while providing more consistent service. Retailers are using similar technology to personalize online recommendations and manage inventory more efficiently, while logistics companies use AI to optimize delivery routes and reduce fuel consumption.

Beyond these sectors, advances in robotics and autonomous vehicles highlight how AI is transforming the physical world as well. In manufacturing, AI-enabled robots are improving precision, speed, and safety on production lines. In transportation, self-driving technology continues to advance as companies test autonomous trucks and cars capable of reducing accidents and improving fuel efficiency. While these technologies are still developing, their potential to alter global supply chains and mobility is significant.

Together, these examples show how AI’s transformation is spreading far beyond technology companies and into the broader economy. Each sector is using AI in different ways, but the common goal is the same: to increase efficiency, lower costs, and unlock new sources of growth.

Economic Impact

AI adoption is already restructuring the broader economy through its effects on productivity, labor markets, and capital allocation. Automation of routine tasks is boosting efficiency and freeing workers to focus on higher-value responsibilities, but it is also displacing certain roles, particularly in entry-level or repetitive functions. For example, recent data shows that demand for some junior programming and support positions has softened as AI is now able to handle basic coding and IT support functions. At the same time, new opportunities are emerging in areas such as data science, systems engineering, and AI model management. These shifts highlight the need for ongoing reskilling and workforce adaptation as adoption of technology increases. The speed of AI adoption appears to be faster than any previous technological revolutions and risks a more acute and painful economic transition for those disrupted by AI technology.

From a macroeconomic standpoint, AI has the potential to lift GDP growth and long-term productivity as businesses use it to operate more efficiently and innovate faster. However, the transition may bring uneven effects across sectors and regions, with varying impacts on wages, job creation, and inflation. For policymakers, the key challenge lies in encouraging innovation without leaving parts of the economy behind, requiring sustained focus on education, infrastructure, and effective regulation.

The recent bull market highlights both the opportunities and risks tied to AI. The “Magnificent 7” stocks, particularly Nvidia, have seen earnings growth outpace even lofty valuation gains, while other AI-focused companies have benefited from strong investor enthusiasm. As adoption expands, the beneficiaries may broaden beyond today’s market leaders, with potential upside for companies outside the top technology giants. At the same time, the surge in AI-related capital expenditure has raised questions about sustainability and if the mega-cap technology firms will realize a sufficient return on their investments, as spending on data centers, semiconductors, and infrastructure reaches record levels. While this wave of investment supports near-term growth and innovation, it has also contributed to speculation about whether current valuations and spending levels are justified, underscoring the uncertainty that often accompanies major technological shifts.

Conclusion

The progression through the Foundation, Platform, and Transformation phases is not a linear sequence of events but a continuous, self-reinforcing cycle. Advances in infrastructure unlock new capabilities, which in turn drive demand for even more computational power for more complex tasks. While the technology is already reshaping productivity and labor markets, the line between speculative hype and durable economic value is still being drawn.

As the landscape matures over time, the market focus will shift from the companies building the models and infrastructure for AI to ones who are capable of effectively monetizing them. The winners of the future will likely be those who move beyond AI adoption to full integration of AI into the core of their business models. In this evolving environment, diversification across industries and geographies remains essential, helping investors and companies manage risk while navigating the ever-expanding and evolving AI landscape.

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor. The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur. For additional information, please visit:https://verumpartnership.com/disclosures.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information and it should not be relied on as such

Be the First to Know

Sign up for our newsletter to receive a curated round-up of financial news, thoughtful perspectives, and updates.

"*" indicates required fields