Perspective in a Time of Conflict: Iran 2026

On February 28th, 2026, the United States and Israel launched joint military strikes against Iran in what the administration has called “Operation Epic Fury.” As we digest these developments, we want to share a few thoughts on the current situation, offer some important historical context, and discuss what we are seeing in the markets.

The 2026 Iran conflict is now in its fourthweek, with no clear resolution timeline and the potential to continue for an extended period.

The strikes have targeted military assets, Iranian leadership, and Iran’s nuclear program. Iran’s Supreme Leader, Ayatollah Ali Khamenei, was killed in the opening strikes.

Iran has retaliated with missile and drone strikes against Israel, U.S. bases in the Gulf, and several of our regional allies. The conflict has expanded to include renewed hostilities between Hezbollah and Israel, as well as attacks on other U.S.-allied targets in the region.

The Strait of Hormuz — the narrow waterway through which approximately 20% of the world’s daily oil supply flows (Source: U.S. EIA) — has been effectively closed to tanker traffic, creating one of the largest oil supply disruptions on record. Additional Iranian attacks on oil infrastructure in the region have further limited supply raising questions around the long-term economic impact the escalating Iran conflict.

What We Don’t Know

As with any major geopolitical event, the list of unknowns is long.

- We do not know how long this conflict will last. The administration has offered varying timelines and objectives, and the situation remains fluid.

- We do not know how long the Strait of Hormuz will remain disrupted, nor how quickly global oil supply chains could normalize once the conflict ends. There are some alternative routes available. Saudi Arabia has the East-West pipeline to the Red Sea port of Yanbu, which, together with the UAE’s pipeline to Fujairah, could provide about 4.7 million barrels per day of bypass capacity (Source: U.S. EIA). Even so, these routes could collectively handle only a portion of the crude that normally flows through the Strait (Source: U.S. EIA). This infrastructure remains within range of potential Iranian strikes, meaning these backup routes are also at risk. There are ongoing discussions about U.S. naval escorts and a broader international coalition to help reopen the Strait to commercial shipping, though those efforts remain in the early planning stages. These developments are worth watching, but for now, these alternatives provide only a partial solution and are unable to replace the full volume that normally transits through the Strait of Hormuz.

- We do not know the full extent of the inflationary impact on the U.S. economy, nor how the Federal Reserve will respond. The Fed faces a difficult dilemma: rising inflationary pressure from energy prices on one side, and the need to support economic growth amid weaker recent jobs data on the other.

What we do know is this: Uncertainty is not new. Markets have navigated wars, oil shocks, financial crises, and pandemics, and the pattern has been remarkably consistent. The short term may be volatile and painful, but over the long term, disciplined investors have historically been rewarded.

Historical Context: Markets and Military Conflicts

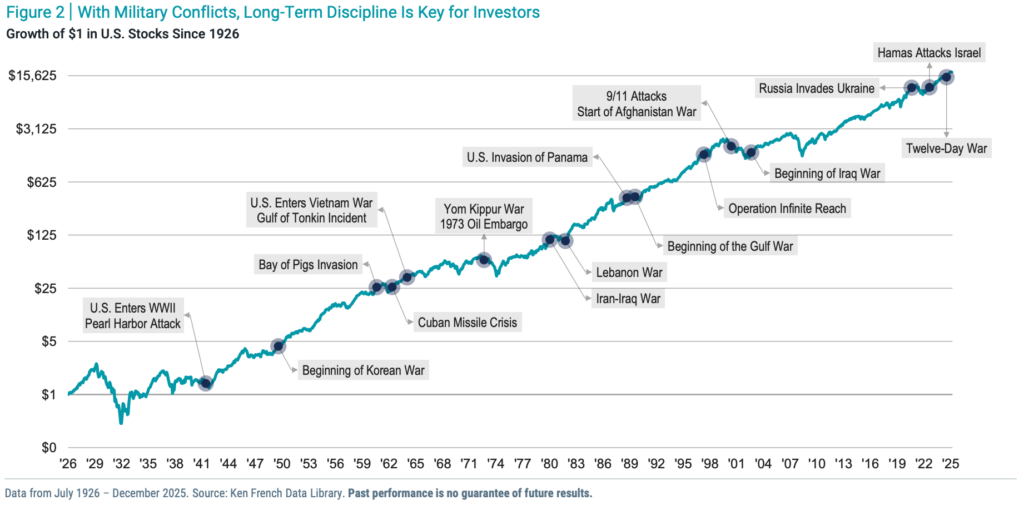

While it is tempting to react to the headlines and sell assets, the historical record provides a powerful counterpoint. The chart below shows the growth of $1 invested in U.S. stocks since 1926, with major military conflicts marked along the way. The message is clear: conflicts cause short-term turbulence, but the long-term trajectory has been resilient.

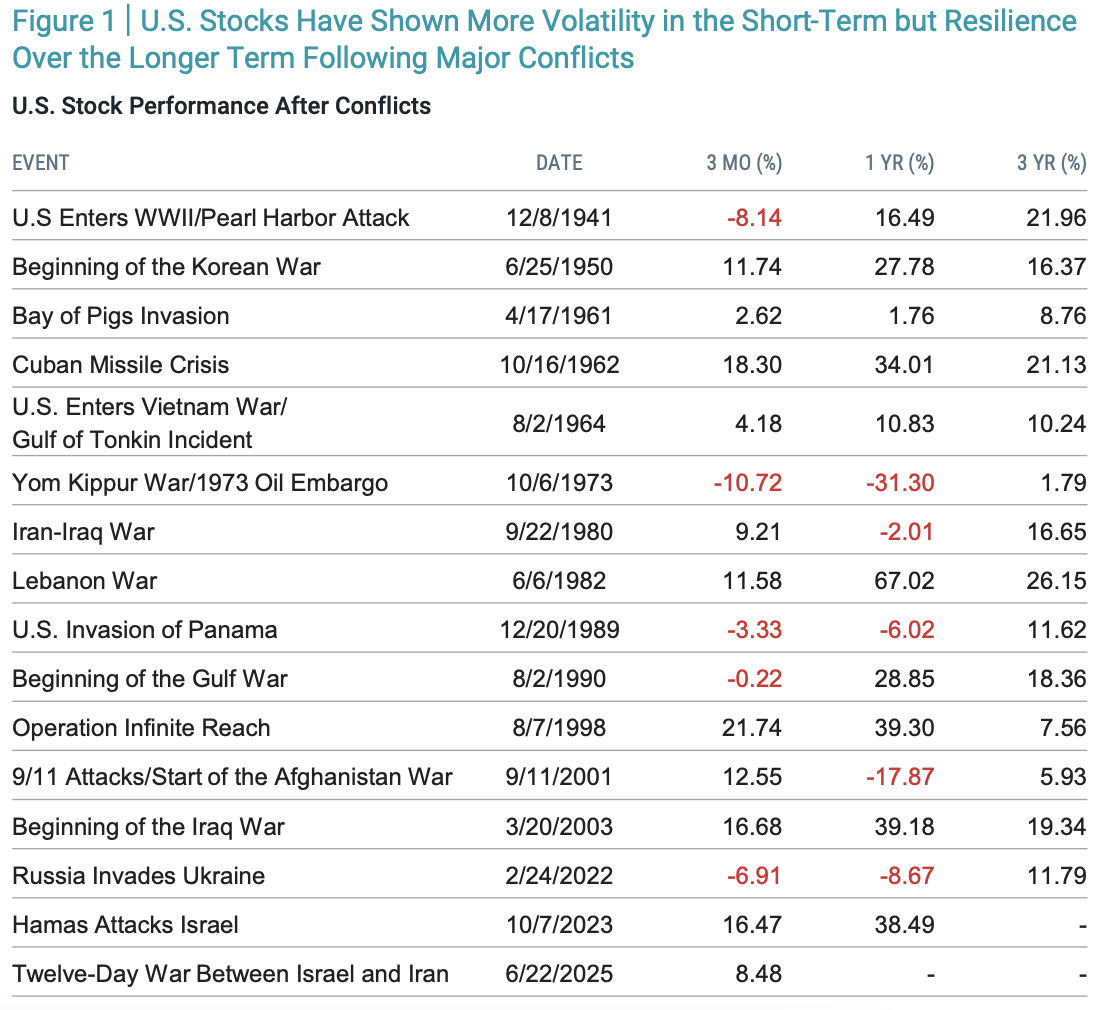

The table below shows U.S. stock performance following 17 major military and geopolitical events since World War II. While the 3-month returns are mixed, reflecting the kind of volatility we are experiencing right now, the 1-year and 3-year returns are overwhelmingly positive.

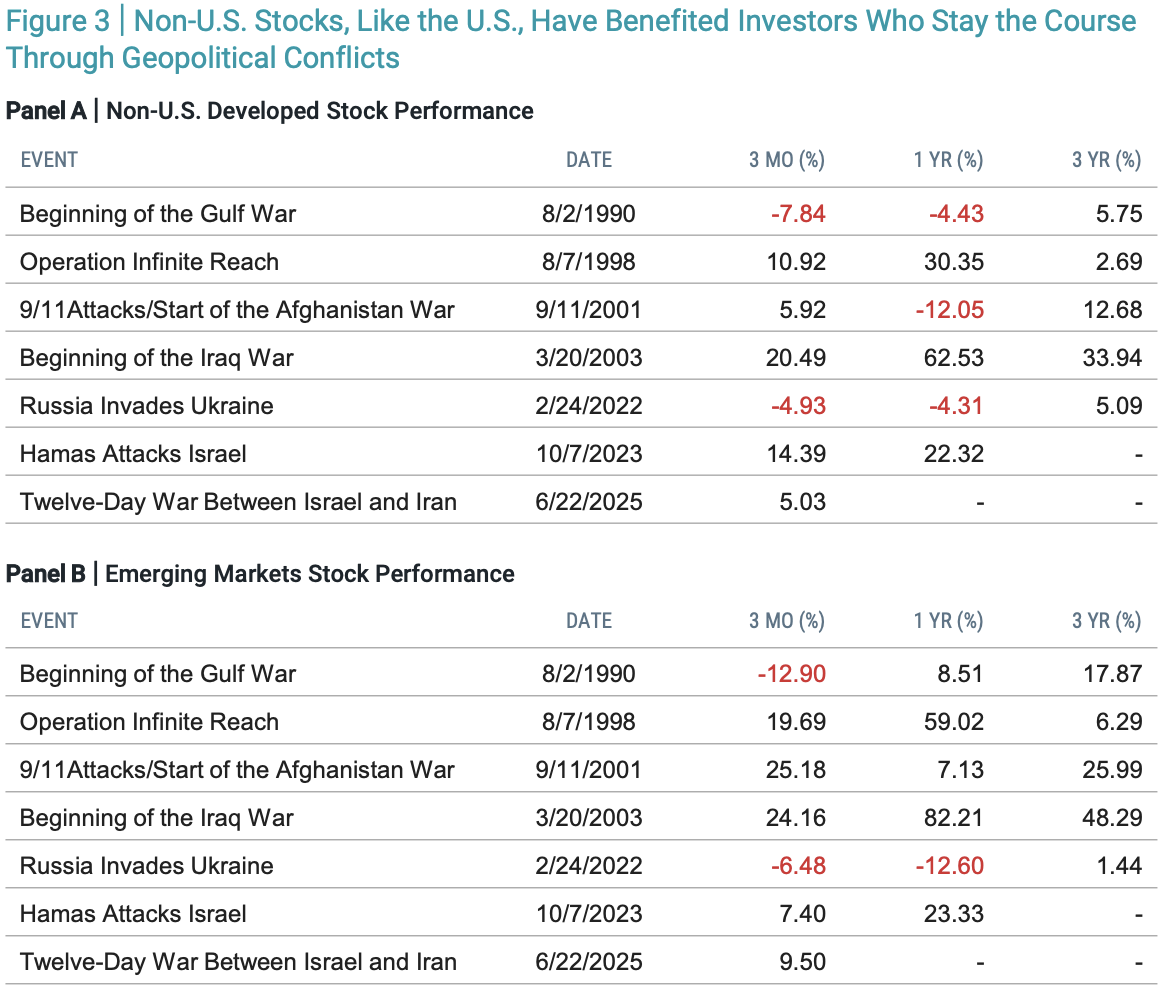

Importantly, this resilience is not limited to U.S. stocks. For investors with globally diversified portfolios, it is just as important to consider how international markets have responded to geopolitical conflict. Non-U.S. developed and emerging market stocks have shown similar patterns of short-term disruption followed by long-term recovery. Over time, investors who stayed the course through geopolitical turbulence were rewarded across global markets as well.

A Few Points Worth Emphasizing

- Of the 17 conflicts shown, only a handful produced negative 1-year returns. Even in those cases, the 3-year returns were positive.

- The most relevant historical comparison may be the Yom Kippur War and the 1973 Oil Embargo, which also involved a major oil supply disruption and triggered an inflationary spike and economic recession. However, the conflict and embargo alone did not account for the severity of the market decline. The Nifty Fifty had dominated market returns in the years prior and were trading at extreme valuations heading into the crisis (Source: Morningstar). Additionally, the end of the gold standard was still reverberating through the financial system, and inflationary pressures were building well before the embargo began (Source: Federal Reserve History). The war and oil shock were the catalyst, but it was the combination of geopolitical disruption and pre-existing market vulnerabilities that made the damage so severe.

- A similar dynamic played out following the September 11 attacks. The 1-year return following 9/11 was sharply negative, but the attacks did not strike a healthy market. The dot-com bubble had already burst, the Nasdaq had fallen roughly 60% from its March 2000 peak, and the economy was already in recession before the attacks occurred (Sources: Federal Reserve Bank of St. Louis; National Bureau of Economic Research; Goldman Sachs). Technology stocks that had driven the market’s historic run-up were still repricing to more reasonable valuations. The attacks added geopolitical uncertainty to a market that was already working through the unwinding of the dot-com bubble. It was that combination of factors, not the conflict alone, that worsened the market’s 1-year return.

- It is worth acknowledging some parallels between those periods and today. A narrow group of technology-driven stocks has led the market in recent years, much as the Nifty Fifty did in the early 1970s and a handful of high-flying tech stocks did in the late 1990s. Artificial intelligence, like the rise of the computer and the internet before it, has fueled significant growth and investor enthusiasm, and valuations were elevated heading into this conflict. This does not mean the outcome will be the same, but starting conditions matter, and markets can be more vulnerable to shocks when leadership is concentrated and valuations are stretched.

- That said, the circumstances around energy are meaningfully different today. In 1973, OPEC controlled roughly 75% of world oil trade (Source: Baker Institute) and outright refused to sell to the United States, leading to severe shortages. Today, the U.S. produces far more oil domestically, maintains strategic petroleum reserves, and has access to non-Middle East suppliers (Source: U.S. EIA). The economy is also more energy efficient, less dependent on manufacturing, and supported by alternative energy sources. Oil prices will likely continue to rise while the Strait remains contested, but the tools available to manage disruptions are considerably stronger than they were 50 years ago, and even severe oil shocks have historically faded with time.

- History does not guarantee future results, but it provides essential perspective. Markets have survived every one of these events, and long-term returns have dwarfed the short-term drawdowns and volatility spikes.

What We’re Seeing in Markets Right Now

Oil Prices

- Brent crude has surged from approximately $73/barrel before the conflict to over $112/barrel as of March 20th, representing a roughly 53% increase in just three weeks (Source: Trading Economics).

- The effective closure of the Strait of Hormuz is the primary driver. Approximately 20% of the world’s daily oil supply transits through this chokepoint, making this an extraordinary supply disruption (Source: U.S. EIA).

- The International Energy Agency (IEA) has announced the largest-ever coordinated release from strategic reserves (400 million barrels), which may help moderate prices in the near term (Source: IEA.) However, the disruption will persist as long as the Strait remains contested.

Inflation and the Federal Reserve

- The oil shock is reigniting inflation concerns. U.S. inflation stood at 2.4% in February, above the Fed’s 2% target, and the energy shock could push it meaningfully higher. The Fed raised its own inflation forecast at its March meeting, now projecting 2.7% for the year, up from 2.4% just three months ago (Sources: U.S. Bureau of Labor Statistics; Federal Reserve).

- The broader growth picture has also softened considerably. The Atlanta Fed’s GDPNow model estimated Q4 2025 growth above 5% in early January, but actual GDP came in at just 1.4%. The Q1 2026 estimate has also declined, falling from 3.1% on February 20th to 2.3% as of March 19th (Sources: Atlanta Fed GDPNow; U.S. Bureau of Economic Analysis).

- The labor market has weakened as well. The economy lost 92,000 jobs in February, significantly more than expected, and average monthly job gains in 2025 were revised down to just 15,000 (Source: U.S. Bureau of Labor Statistics).

- This puts the Federal Reserve in a difficult position. The Fed held rates steady at 3.5%–3.75% (Source: Federal Reserve) at its March meeting, and Chair Powell acknowledged that the economic impact of the conflict remains unclear. Higher oil prices may keep inflation elevated, while weaker growth and employment argue for supporting the economy. The path for rate cuts has become considerably less clear, with most officials still projecting one cut this year, but the timing is increasingly uncertain (Source: Federal Reserve, March FOMC materials).

Bond Yields

- The 10-year Treasury yield was 3.97% on Friday, February 27, before rising to 4.05% on Monday, March 2, and stood at 4.39% on Friday, March 20th as inflation concerns intensified (Source: U.S. Department of The Treasury).

- Higher yields increase borrowing costs across the economy and put downward pressure on stock valuations, with smaller companies typically feeling more strain than large caps.

Equities

- Broad equity weakness alongside higher oil prices is consistent with past geopolitical episodes, when markets often experience a period of short-term repricing and higher volatility.

- U.S. equities have pulled back since the conflict began, but the decline has so far been more measured than some other recent market shocks. As of March 20th, the S&P 500 is down 4.68% year to date (Source: Conway Investment Solutions).

- Outside the U.S., international developed and emerging market stocks may face added pressure from higher energy costs and weaker global growth, especially in regions that rely more heavily on imported energy. As of March 20th, the MSCI EAFE index is down1.41%year to date and the MSCI Emerging Markets index is up 4.52% year to date (Source: Conway Investment Solutions).

- Overall, the market reaction has been driven by rising oil prices, inflation fears, and broader risk-off sentiment. Energy stocks have been a notable beneficiary, but the broader equity market remains under pressure.

Portfolio Implications

- Diversification remains key. The S&P 500 is often thought of as a broadly diversified portfolio, but today its top two sectors account for roughly 44% of the index, while energy represents less than 4% (Source: YCharts). That kind of concentration can leave investors overexposed to the sectors under pressure and with very little allocation to the ones that benefit during periods like this. True diversification means building portfolios with healthy exposure across asset classes, geographies, and sectors, not relying on an index where a handful of stocks and one or two sectors drive the majority of returns.

- Market dislocations create opportunities for disciplined investors. If high-quality assets are selling off due to fear rather than fundamental deterioration, those with properly diversified portfolios should be prepared to rebalance into weakness.

- As the historical data shows, the bigger risk to long-term financial success is often not the conflict itself but reacting too strongly to it. Making major all-in or all-out investment decisions based on emotion, rather than staying grounded in a plan, has historically been far more costly than the event itself.

Wrap Up

During times like this, the headlines can feel overwhelming, but history reminds us that uncertainty is a normal part of investing. While the road ahead may remain volatile in the near term, staying diversified, disciplined, and focused on long-term goals has historically served investors far better than reacting to short-term headlines.

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor. The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur. For additional information, please visit:https://verumpartnership.com/disclosures.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information and it should not be relied on as such

Be the First to Know

Sign up for our newsletter to receive a curated round-up of financial news, thoughtful perspectives, and updates.

"*" indicates required fields