Liberation Day – Let the Trade Games Begin, May the Odds Forever Be in Your Favor

On April 2, 2025, President Donald Trump announced the most sweeping tariffs on U.S. trading partners in over a century, marking the official start of a large-scale trade war. The U.S. now finds itself engaged in economic conflict with nearly 60 countries. As we digest all of this we want to share a few thoughts on the rapidly escalating trade tensions, including our current thinking on the administration’s desired outcome and the risks associated with the approach. Stay tuned to the end where we share portfolio implications and some other reading we recommend for more perspective.

- Following the election outcome in November, markets began to react to the “Trump Trade” or the “Trump Bump.” Market action focused on clear winners and losers. The winners were U.S. stocks that could benefit from lower taxes and easing regulations such as financials, energy, and technology stocks. Interest rates went higher on the news and the U.S. dollar continued to appreciate against most other major currencies. This led to negative returns for international stocks and poor results for bonds.

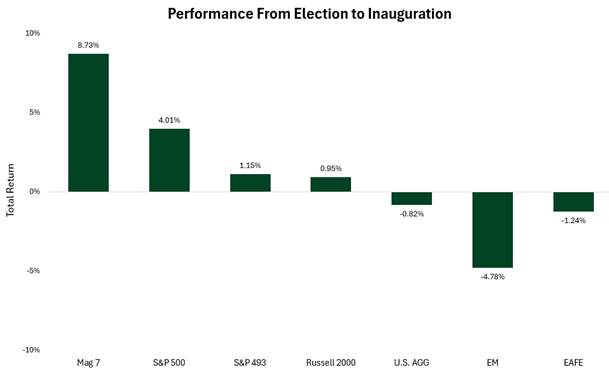

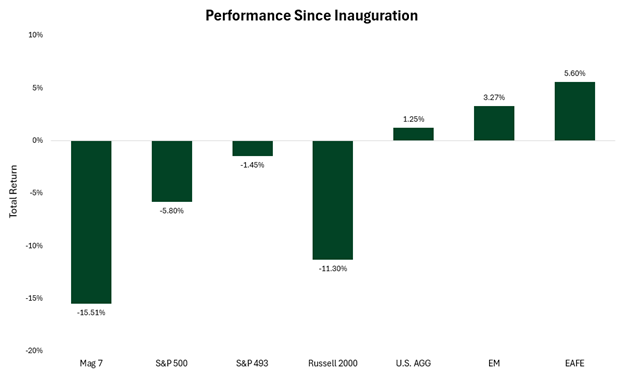

- Since President Trump took office in January 2025, market leadership trends have completely reversed. The charts below illustrate asset class performance from election day to inauguration day, as well as from inauguration day to what the administration is now calling “Liberation Day.” Note that it does not include April 3rd market action.

- Emerging markets and international stocks, once anticipated to be among the losers following the election, have instead outperformed U.S. stocks, aided by a weakening U.S. dollar. Bond prices have shifted from negative to positive. Meanwhile, the widely discussed “Magnificent Seven” stocks in the S&P 500 have fallen from market leaders to the worst performers. Did the market just get this wrong? Was it expecting a different Trump presidency? It is hard to say whether the market was actually wrong, but we believe the market is a bit surprised that the president is not more focused on the performance of the stock market. During his first term, Trump frequently highlighted the stock market’s performance in tweets, speeches, and public statements. In contrast, his second term has seen little mention of the stock market, and in fact, he has publicly disregarded it.

- Why the change? What is the point of the tariffs and what is the Trump administration trying to accomplish? While we do not ultimately know what the “grand plan” might be, there are some particularly important clues we think are worth paying attention to:

- In November 2024, Senior Strategist at Hudson Bay Capital, Stephen Miran, penned a document titled “A User’s Guide to Restructuring the Global Trading System.” Stephen Miran is now the Chair of Donald Trump’s Council for Economic Advisors. His paper is premised on the idea that the U.S. manufacturing base has largely evaporated due to the current trading system. Since the U.S. furnishes the U.S. dollar as the reserve currency for the rest of the global trading system, the dollar is systematically overvalued, in Miran’s view. A strong dollar has meant that the U.S. struggles to be competitive in manufacturing with other countries. Mr. Miran’s theory is the political unrest that has led to populist uprisings in support of Donald Trump (we would argue that other populist movements, including the rise of Bernie Sanders, stem from similar origins) come from economic imbalances that are rooted in dollar overvaluation. His “user guide” effectively lays out the following framework to course-correct:

- Implement tariffs to create economic strain on trading partners. Force trading partners to the table and cut both multilateral and more often unilateral agreements whereby trading partners agree to engage in currency manipulation to weaken the U.S. dollar and maintain a weaker dollar.

- Additionally, multiple White House officials, including Treasury Secretary Bessent, have alluded to concerns over the U.S. fiscal issues and have suggested that interest rates will need to fall. If interest rates were to fall, it could do two things:

- Allow the Treasury to consolidate U.S. debt into long-term bonds at lower rates than current levels.

- Help weaken the U.S. Dollar, given that U.S. interest rates remain high relative to other Western nations.

- Jim Bianco of Bianco Research has a combined theory in which there is a grand plan to lower interest rates and weaken the dollar through strategic deals with key trading partners. The deals would be structured to provide trading partners free and unlimited access to trade with the U.S. in exchange for helping weaken the U.S. dollar’s value, while simultaneously agreeing to buy U.S. long-term debt at very low rates. Mr. Bianco has dubbed this the “Mar-a-Lago Accord.”

- In November 2024, Senior Strategist at Hudson Bay Capital, Stephen Miran, penned a document titled “A User’s Guide to Restructuring the Global Trading System.” Stephen Miran is now the Chair of Donald Trump’s Council for Economic Advisors. His paper is premised on the idea that the U.S. manufacturing base has largely evaporated due to the current trading system. Since the U.S. furnishes the U.S. dollar as the reserve currency for the rest of the global trading system, the dollar is systematically overvalued, in Miran’s view. A strong dollar has meant that the U.S. struggles to be competitive in manufacturing with other countries. Mr. Miran’s theory is the political unrest that has led to populist uprisings in support of Donald Trump (we would argue that other populist movements, including the rise of Bernie Sanders, stem from similar origins) come from economic imbalances that are rooted in dollar overvaluation. His “user guide” effectively lays out the following framework to course-correct:

Thoughts and Implications

- If the Mar-a-Lago Accord theory is truly what the White House is trying to achieve, it will be the single riskiest economic policy undertaking in modern United States history.

- Tariffs are ultimately a tax. The tax is not on foreign countries but have to be absorbed by either the end consumer (higher costs) or by companies producing and selling the goods through lower profitability. (Depending on the industry, tariffs will cause loss absorption to be spread in different and often unequal ways across the supply chain of companies who produce the good or service).

- We estimate that in the early innings of a trade war, prices of goods and services will likely adjust higher, and inflation will be persistent. This could create a scenario in which interest rates also move higher and potentially lead to a period of stagflation.

- However, eventually (could be days, weeks, months, or years), demand shrinks for the good and thus you have a scenario in which prices could actually be lower but economic activity and the totality of goods and services exchanged go down.

- Regardless of whether this will end in inflation or deflation, there is no denying that tariffs shrink the pie of the economy. They are anti-growth in every way, shape, and form. The extent to which they contract the economy and create a recession will ultimately hinge on the duration and magnitude of the tariffs, and Americans will need to look for clues from the White House to determine just how bad this will be in the near term.

Portfolio Implications

- Since the Great Financial Crisis, the U.S. stock market, and particularly the large company U.S. stock market (S&P 500), has had its single best return period on record and has led all developed and emerging countries. This long-term bull market (we had bear markets in 2020 and 2022 that were short lived) has culminated in a highly concentrated market in which just seven stocks have produced a substantial amount of the bull market returns from 2022 to the end of 2024.

- We believe the rather extreme market dislocation of those seven stocks relative to the rest of the corporations across the globe may be correcting course.

- What worked over the last 15 years may not work as well going forward. If Mr. Miran penned the user’s guide to restructuring the global trading system, we will take a quick stab at a user’s guide to living through the Mar-a-Lago Accord:

- Diversification will be the key. Investors who have too much U.S. dollar and U.S. stock exposure may be at risk the most. International stocks and non-U.S. dollar assets should provide diversification benefits, including mitigating the risk of outsized exposure to a weaker dollar.

- Diversifying into bonds – The bond market is a very unloved asset class right now. This is because of recency bias as bonds have experienced their worst three-year return on record. But interest rates ended 2021 at historically low levels, and, today, investors can buy bonds with positive real returns. Investors who are willing to buy bonds with longer maturities than T-bills or cash can lock in the current interest rates for years to come, and if rates were to drop rapidly those investors should receive major price appreciation. In short, we believe bonds are a necessary component of diversification and provide asymmetric upside opportunities.

- Interest rate sensitive assets (within Offense) – Since the 2022 rise in interest rates, several equity sectors have performed quite poorly due to concerns these sectors will generate lower returns on capital due to higher rates. What sectors? Those with high leverage, like real estate, utilities, and consumer staples, but also including smaller growth companies that might have a disruptive business model but do not have the free cash flow to weather a higher rate environment. We believe that investors should look to diversify into both value stocks and smaller cap stocks to take advantage of lower interest rates. There could be economic pain ahead for these types of investments but current valuations on small cap and value stocks are substantially more attractive today than large cap growth stocks.

- Ultimately, we don’t know how this economic experiment will end. But we do believe the chances of a recession have meaningfully risen and, while segments of the market are down substantially, we are still in a correction and not a bear market. Investors with too much risk should consider diversifying and decreasing risks to match their long-term goals. Investors with properly diversified portfolios should ensure they have a plan for rebalancing as markets evolve and take advantage of weakness in high quality Offense assets.

- Regardless of what happens, history teaches us that: businesses will find ways to adjust to new environments, bear markets tend to be much shorter than bull markets, and investors who diligently save money into broadly diversified portfolios are often handsomely rewarded with the compounded returns they receive over many years. The best way to fail at a financial plan is to go all in and all out based on how you are feeling. We may be heading into uncharted territories, but removing your capital from the markets altogether and waiting until seas have calmed has historically been very costly.

If you’re interested in more perspectives, here are some of the thoughtful and objective voices we’re reading:

Callie Cox on LinkedIn, sharing perspective on escalating trade tensions and tariffs

Sam Ro in his Substack, writing on the stock market’s history with recessions

Spencer Jakab in the Wall Street Journal, reminding us of valuation differences between U.S. and international stocks and how that impacts investors

Michael Batnick on his blog, with perspective on changing consumer confidence, the market’s interpretation of “Liberation Day,” and what disciplined investors do moving forward

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor. The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur. For additional information, please visit: https://verumpartnership.com/disclosures/

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

Be the First to Know

Sign up for our newsletter to receive a curated round-up of financial news, thoughtful perspectives, and updates.

"*" indicates required fields